I've seen this before - the Bitcoin market can be unpredictable and prone to sudden changes. Back in 2017, the price of Bitcoin skyrocketed to nearly $20,000, but what many newcomers don't realize is that the market has changed significantly since then.

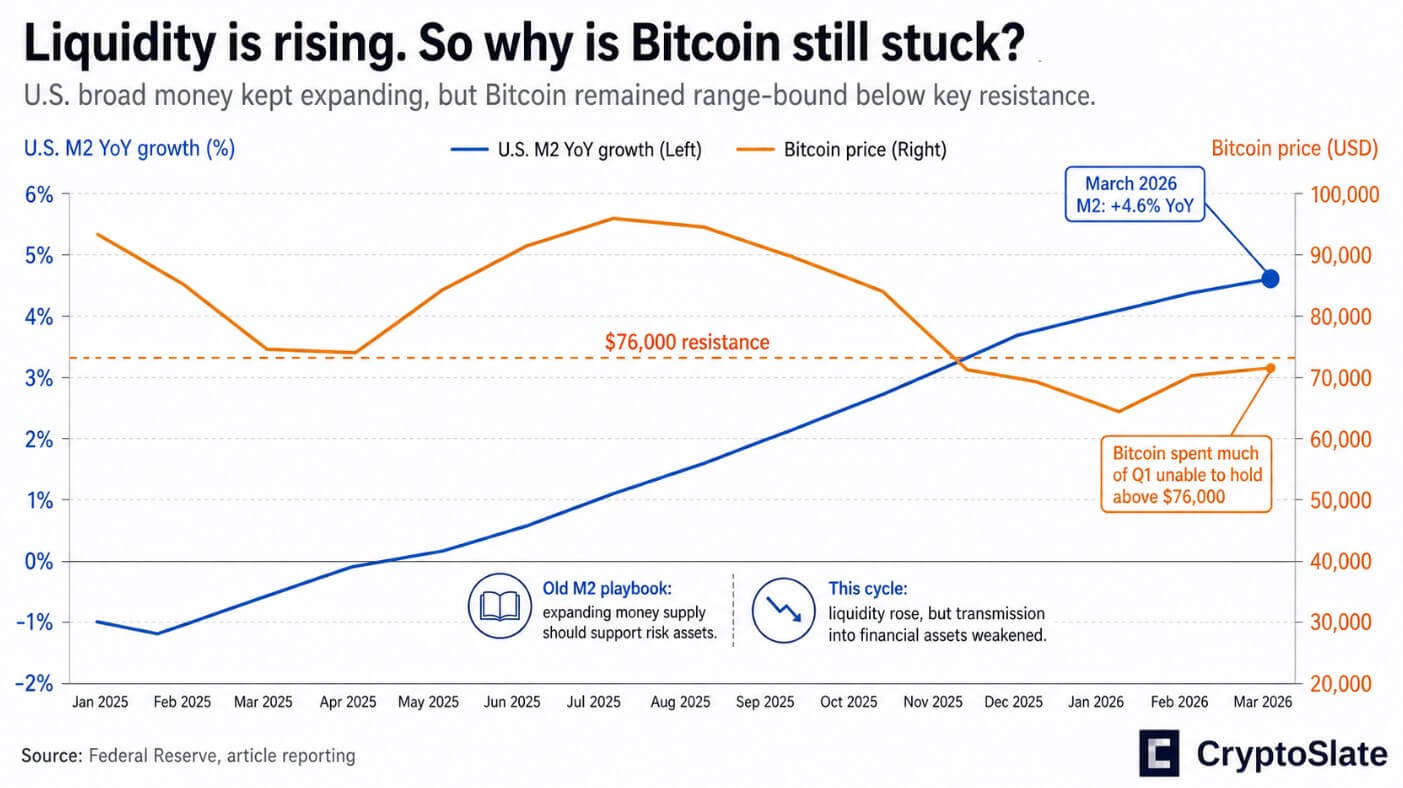

The old Bitcoin playbook ran on the simple logic that when global M2 expands, capital flows into risk assets, and Bitcoin captures a disproportionate share. However, this relationship has broken down, and the global M2 has been expanding while Bitcoin has continued to underperform. What's behind this change? The answer lies in the gap between debt and liquidity.

The Gap Between Debt and Liquidity

The US public debt has closed the fourth quarter of 2025 at over $38.5 trillion, up 6.3% year over year. Meanwhile, US M2 grew by 4.6% over the same period. Based on the most basic numbers available, debt is outpacing broad money by nearly two percentage points annually. The debt stock now equals roughly 1.70x total M2, a ratio with no modern precedent in a supposedly accommodative monetary environment.

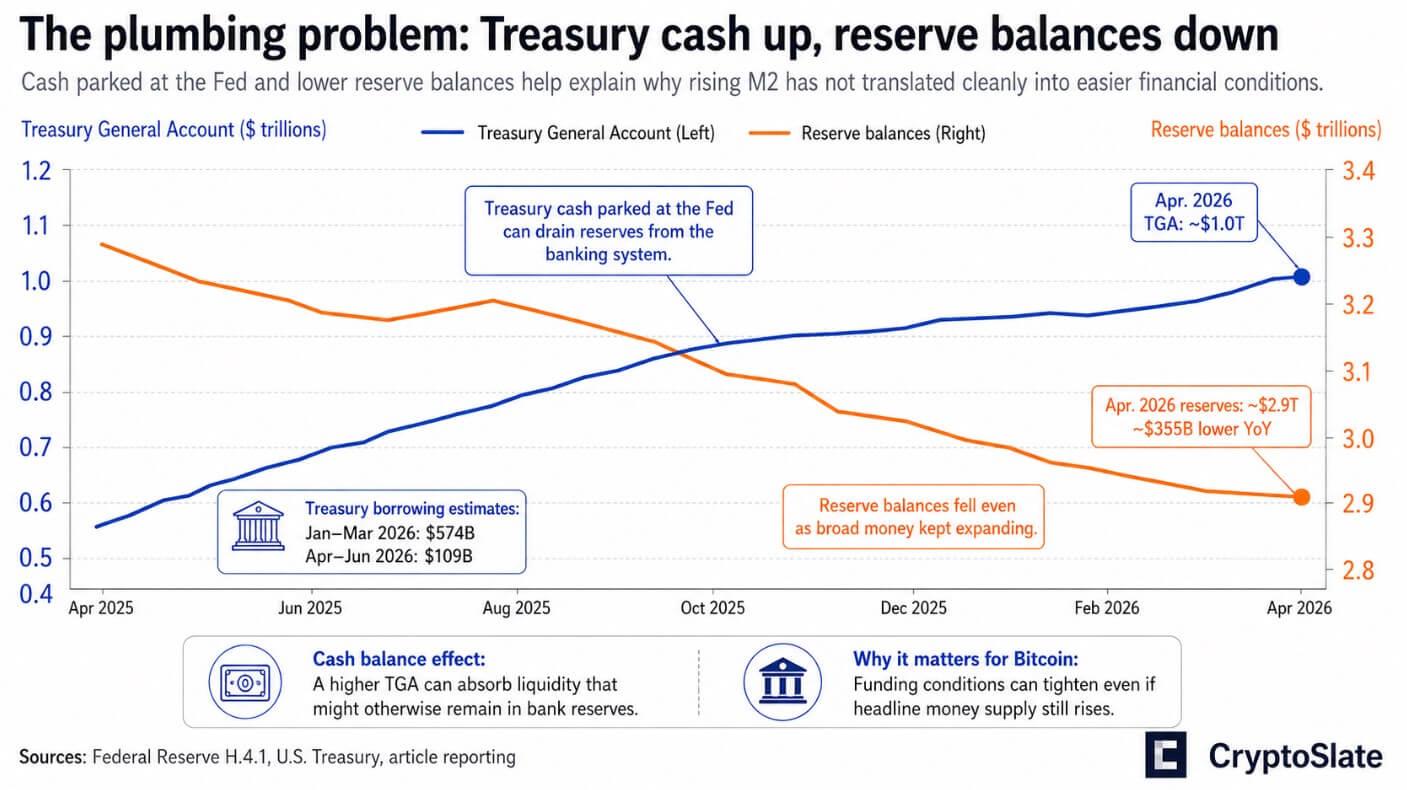

- The Treasury's own borrowing estimates called for $574 billion in net marketable debt in the January-March 2026 quarter and another $109 billion in April-June, while maintaining a cash balance above $1 trillion.

- The Treasury General Account, which sits at the Federal Reserve, held roughly $1 trillion in the latest H.4.1 data. Cash parked at the Fed drains reserves from the banking system even as M2 continues to tick up.

- Reserve balances fell to about $2.9 trillion in the Fed's Apr. 22 release, down approximately $355 billion from a year earlier.

Why the Old Chart Broke

Coutts argued on the podcast that Bitcoin's underperformance reflects plumbing friction. The selloff from late 2024 into early 2025 drew on tightening reserve conditions in the fourth quarter, Treasury dynamics tied to a government shutdown, derivatives-driven deleveraging, and the expanding role of ETF and derivatives markets in Bitcoin's price structure.

None of these forces appear in a global M2 overlay, as they are features of a financial system in which Treasury supply, reserve management, and funding conditions have become the real battleground. Gold offers the clearest cross-market confirmation. Central banks bought 244 tonnes of gold in the first quarter, up 3% year over year, with total gold demand reaching 1,231 tonnes and a record $193 billion by value, per the World Gold Council.

Two Outcomes

In the bull case, inflation cools toward the Fed's projected path, the Treasury cash balance declines, reserves rebuild, and bank credit continues to expand without a growth scare. In that setup, the "liquidity is still expanding" thesis regains traction. Bitcoin can re-rate quickly because the debt-to-liquidity mismatch prevents the tightening of financial conditions at the margin.

In the bear case, debt issuance stays heavy, inflation stays sticky, Treasury funding strain persists, and the Fed cannot ease without reigniting the inflation it has spent two years suppressing. Bitcoin then behaves less like a monetary hedge and more like a high-beta risk asset exposed to rates, funding conditions, and periodic deleveraging.

Our Take

As a battle-tested crypto veteran, I've seen the market go through multiple cycles. The key to success in crypto is not to get caught up in the hype, but to focus on the fundamentals. The gap between debt and liquidity is a significant risk factor that investors should be aware of. While the bull case is possible, the bear case is more likely, and investors should be prepared for sharp drawdowns and frustrating consolidations.

It's time to take a step back and re-evaluate the market. The old playbook is no longer applicable, and it's time to adapt to the new reality. As I always say, "it's not about being right, it's about being prepared".