I've seen this before - the hype surrounding a new development in the crypto news space, only to be followed by a sobering reality check. Back in 2017, I was skeptical of the bitcoin price surge, but as I dug deeper, I realized that the underlying fundamentals were solid.

What many newcomers don't realize is that the web3 news and cryptocurrency markets are highly cyclical. The current battle between banks and crypto companies over stablecoin yield on the Clarity Act is a prime example. Coinbase's new credit fund, CUSHY, is a direct bet that stablecoins are mature enough to serve as distribution rails for institutional credit.

The Blockchain News and Finance News Landscape

The launch of CUSHY is a significant development in the crypto hot topics space, as it offers investors access to the structural alpha from tokenization, protocol incentives, and on-chain market structure. However, the credit risk survives the wrapper, and the difference between the wrapper's apparent liquidity and the asset's actual liquidity is a major concern.

Some key points to consider:

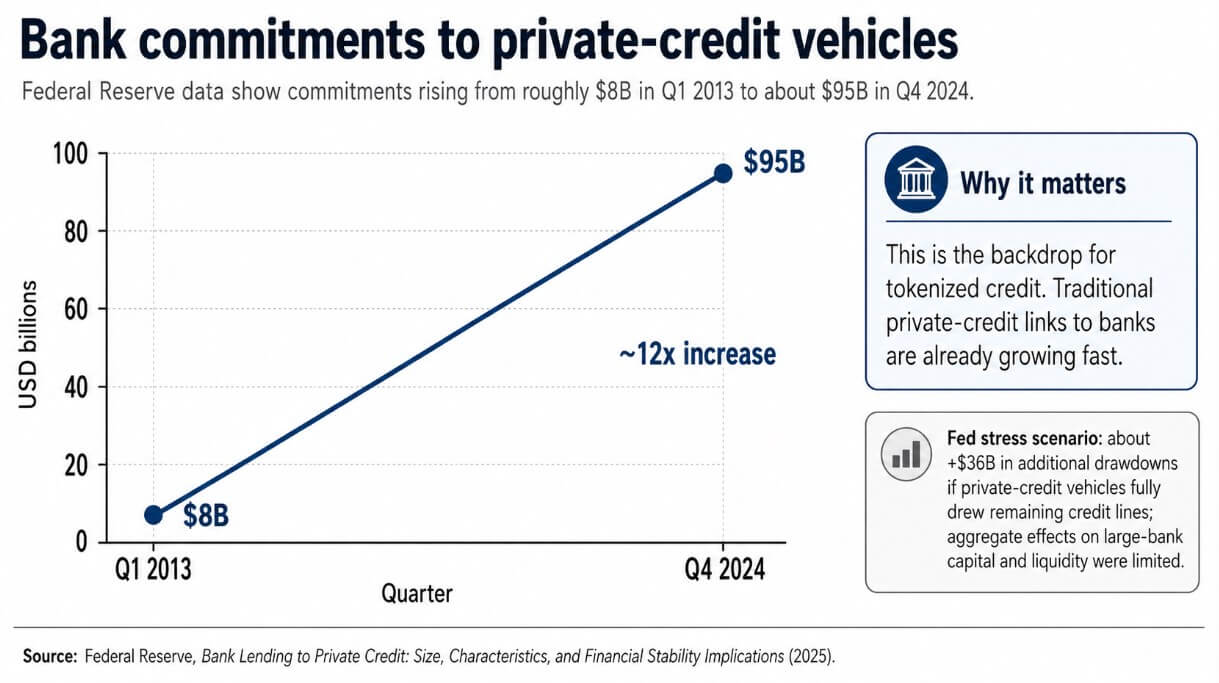

- The Federal Reserve tracks bank commitments to private credit vehicles, which have climbed from roughly $8 billion in the first quarter of 2013 to about $95 billion in the fourth quarter of 2024.

- Coinbase's CUSHY leaves the core tension between digital rail speed and credit market depth intact.

- The direct bank-stability implications appear contained for now, but the Fed also flagged opacity and intensifying interconnectedness between banks and private-credit vehicles as factors warranting close monitoring.

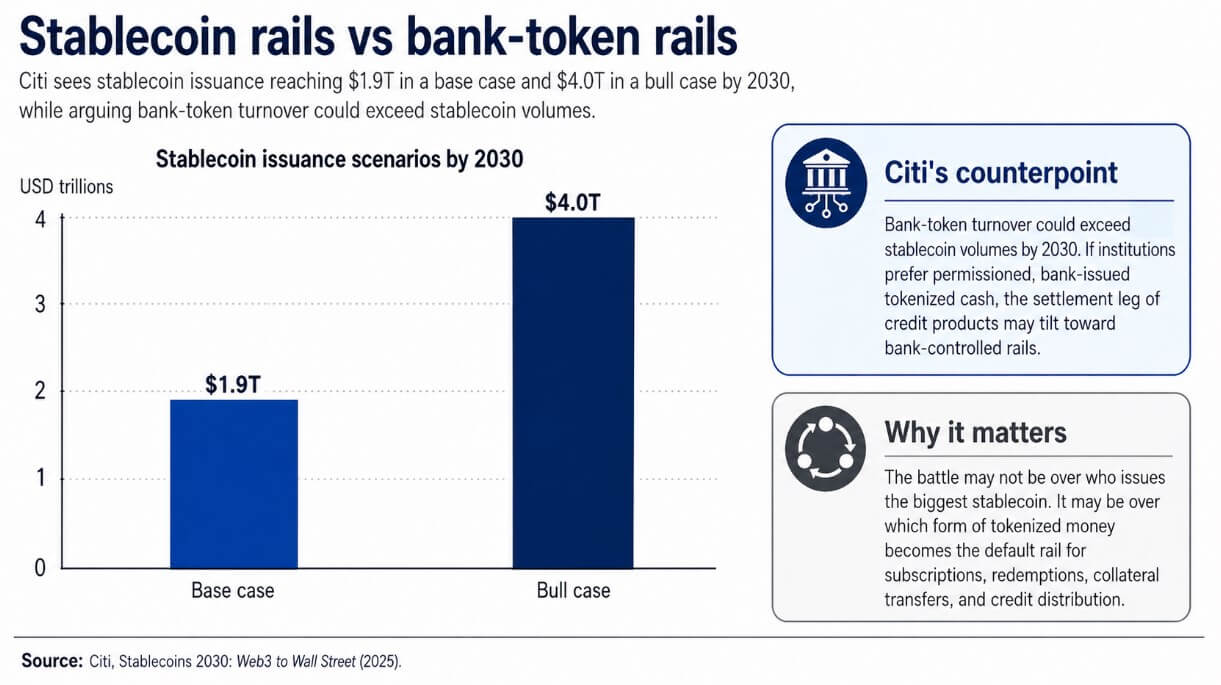

As I look to the future, I'm filled with hope and curiosity. The question now is whether institutional allocators trust public chain stablecoin networks more than the permissioned token systems that large banks are building in parallel.

Our Take

As a battle-tested crypto veteran, I believe that the key to success in crypto blogs and bitcoin investing is not to get caught up in the hype, but to focus on the fundamentals. The launch of CUSHY is a significant development, but it's essential to approach it with a critical and nuanced perspective.

Some potential implications to consider:

- The growth of stablecoin infrastructure could lead to increased adoption of ethereum and other cryptocurrency platforms.

- The development of permissioned token systems by large banks could pose a threat to the growth of public chain stablecoin networks.

- The credit risk associated with stablecoin-infused credit products could lead to increased regulatory scrutiny.